| | |  Business News | October 2008 Business News | October 2008

Global Markets Plunge

David Jolly, Bettina Wassener & Keith Bradsher - The New York Times David Jolly, Bettina Wassener & Keith Bradsher - The New York Times

go to original

Paris - Another wave of relentless selling washed over global markets Wednesday, with stocks plunging in Europe and Asia. The Tokyo market had its worst decline since the 1987 crash.

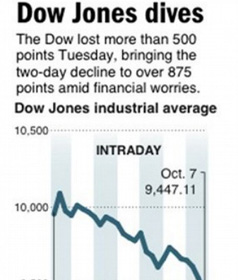

The British government's announcement of a plan to bail out the country's foundering banks with about $88 billion of new capital did little to restore market confidence, with banks again leading indexes lower Wednesday after the Dow Jones industrial average fell 5.1 percent in New York Tuesday.

"It was a horrible session in New York and a horrible session in Tokyo," Jim Reid, head of fundamental credit strategy at Deutsche Bank in London, said. "The momentum is negative."

"I think there are probably more bank failures and forced consolidation to come in the financial sector," Reid said. "Whatever day of the week you wake up, it's another country having problems."

Japanese stocks plunged 9.4 percent Wednesday, leading the Nikkei 225 to at 9,203.32, the lowest since 2003. It was the biggest single-day loss in the index since October 1987. The selloff followed Tuesday's drop of more than 3 percent. The index is now down 40 percent in 2008.

Toyota Motor, Nissan Motor and Honda Motor all fell more than 10 percent on expectations that the global downturn, and particularly the faltering U.S. economy, would hit their results.

In European morning trading, the DJ Euro Stoxx 50 index, a barometer of euro zone blue chips, fell 7.2 percent. The FTSE 100 index in London declined 6.7 percent, the CAC-40 in Paris fell 8.2 percent, and the DAX in Frankfurt fell 7.5 percent.

In Moscow, the Micex index plunged 15.5 percent at the opening and exchange officials suspended trading until Friday.

Britain on Wednesday announced a three-part multibillion-dollar bailout for its beleaguered banks, and Spain moved to mount a separate rescue of its own banking sector.

In Hong Kong, where markets were closed for a holiday on Tuesday, stocks slumped 8.2 percent, despite news that the Hong Kong Monetary Authority had lowered its benchmark interest rate in an effort to bolster bank lending. The move followed interest rate cuts around the world as central banks and governments struggle to contain the spreading financial crisis.

The Shanghai composite index fell 3 percent, and in Seoul, the Kospi fell 5.8 percent. James Chirnside, who manages $65 million at Asia Pacific Asset Management in Sydney, said that investors feared corporate profits would fall and many companies would fail if banks do not resume lending soon. Only a coordinated round of interest rate cuts by central banks around the world is likely to unfreeze interbank lending markets and cause banks to lend more to each other and industrial borrowers as well, he added.

"Without that sort of global coordination, we'll still be hostage to these violent moves in the market," Mr. Chirnside said.

There is as yet little sign of an internationally coordinated interest rate move designed to shore up slowing growth and restore market confidence. But pressure for further easing is growing by the day, and the U.S. Federal Reserve chairman, Ben Bernanke, on Tuesday signaled a readiness to cut rates further, given that the market turmoil could cause U.S. economic activity to be subdued into 2009.

Hans Genberg, the executive director for research at the Hong Kong Monetary Authority, said that even if the Federal Reserve pushes down its overnight interest rate - the Federal Funds rate - financial markets might keep falling and harm to the global economy would not be contained.

"Rate cuts, Federal Funds cuts, are not going to be enough," at a time when banks are reluctant to lend to each other, he said, adding that considerable academic research suggests that the United States must find a way to restore the capital bases of its banks.

Olaf Unteroberdoerster, the International Monetary Fund's representative in Hong Kong, was similarly gloomy about the potential of interest rate cuts to stop the problems. "The key lesson is when you face a confidence issue where the market participants no longer trust each other, the conventional macroeconomic tools are not as effective," he said.

Economists have been gradually reducing their forecasts for economic growth in Asia, and warn that further reductions may be coming soon. "All the risks to those numbers are very much on the downside," said Michael Buchanan, Goldman Sachs' chief economist for Asia except Japan.

Mounting difficulties in European economies are starting to spill over into Asia, where many companies had been trying to step up sales to European consumers before the euro started falling sharply in recent weeks. "For a long time, I think Asia was hoping exports to Europe would make up for a shortfall in the U.S.," Mr. Buchanan said.

Robert Cardarelli, a senior International Monetary Fund economist, said at a press conference in Hong Kong on Wednesday that the fund's recent research showed that during financial crises in which banks are particularly affected, "we are in for a much more severe and protracted downturn."

U.S. crude oil for November delivery fell $2.10 to $87.96 a barrel in electronic trading on the New York Mercantile Exchange.

Plunges in Asian stock markets caused many investors to buy yen, as Japan's well-capitalized banking system appeared to be a refuge from turmoil in financial markets even as the Japanese stock market took heavy losses. The dollar fell at one point below 100 yen - a level that will further hurt the profits of many Japanese industrial companies like Sony and Toyota that depend heavily on sales in the United States.

In Paris morning trading, the dollar had recovered to 100.27 ye but was still down from 101.49 late Tuesday in New York.

The euro rose to $1.3607 from $1.3590 late Tuesday, while the pound rose to $1.7530 from $1.7457.

Indonesia's stock exchange halted trading after a morning plunge of 10.4 percent. The main floor of Jakarta's benchmark stock exchange building fell quiet at about 11 a.m. Wednesday after officials there suspended trading for the first time in eight years. The main Jakarta stock index, the JSX, fell more than 10 percent for the second day in a row, making this one of the worst weeks in 20 years. The last time trading had been suspended here was in 2000, when a car bomb exploded outside the stock exchange building.

"I don't think anyone has seen anything like this in a long time," said Eugene Galbraith, president commissioner of Bank Central Asia.

Exchange president Erry Firmansyah told reporters the suspension would likely last only through the end of the day and was necessary to give investors time to calm their nerves as worldwide economic fears strike Jakarta.

Indonesia has a large export-driven economy closely tied to the economy of the United States. But analysts said despite the current panic here they expected the market to simmer in the coming days.

"Across the board, people are trying to rotate out of the stock market and into a more safe haven," said Gita Wirjawan, the former president director for JPMorgan in Indonesia. "It is to some extent attributable to a bit of panic, the market has some exposure to risk, but it won't be to the extent of China, India or Japan."

Bettina Wassener and Keith Bradsher reported from Hong Kong. Peter Gelling contributed reporting from Jakarta. |

|

| |