| | |  Editorials | Issues Editorials | Issues

Top Economists: The Second Great Depression has Arrived

Terrence Aym - helium.com Terrence Aym - helium.com

go to original

August 27, 2010

David Rosenberg, market guru, has officially declared that the US economy is in a state of depression, and he sees the economic superpowers woes worsening.

On the heels of that bleak forecast, the statistics for existing home sales for July were released and the numbers were ugly. The weak housing market collapsed. Reflecting the worst slump in American history, existing housing sales had plummeted a stunning 27 percent and there's no sign on the horizon that sales will stabilize any time soon.

The bottom line, argues Rosenberg and others: the US economy has collapsed into another Great Depression.

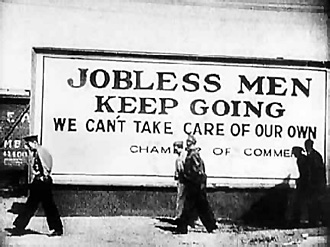

Citing the period from 1929 to 1932 and the eerie similarities, Rosenberg said, "We may well be reliving history here. If you're keeping score, we have recorded four quarterly advances in real GDP, and the average is only 3 percent." The same happened during the early 1930s stock market rebound of 50 percent after the 1929 crash.

The Great Depression followed the brief economic upswing.

As long as two years ago, one of Britain's top economists predicted a decade-long depression, $45 trillion in debt defaults and unemployment in the US and UK approaching 25% or higher.

During October 2008, economist Fred Harrison told the Foreign Press Association in London,""The massive contraction in demand caused by this 'wealth effect' will condemn the western economy to a decade-long depression."

Like some economists who alerted the Clinton and Bush administrations about the approaching economic crisis, Harrison warned future Prime Minister Gordon Brown of the looming financial danger when Brown was appointed Chancellor of the Exchequer in 1997. Brown, like Presidents Clinton and Bush, ignored the warning.

"Brown blames America for the global crisis. But every country in the world permitted property speculation, which is at the heart of boom/busts. Brown now defends himself by claiming that he tried to get global agreement on a stabilization plan. But he failed to tell the other governments about the tax reforms that could have prevented the crisis," Harrison explained in his speech in London.

Two years later, more economists agree with Harrison. Such luminaries as Arthur Laffer and Paul Krugman are two. Although at the opposite ends of the political spectrum, both see dire times ahead for the United States: higher unemployment, a worsening of the credit crisis and housing slump, more loan defaults, more business failures and more foreclosures. Add to this economic witch's brew the possibility of simultaneous currency deflation and inflation and you have every ingredient necessary for another extended Great Depression.

In fact some economists have begun using the term, Great Depression II.

Harrison concurs and believes that the situation has become so serious that whole nations could fail and something unseen in the West for hundreds of years could appear again: wholesale starvation of peoples in some Western countries.

Back in 2008, Spectator Business reported that "Harrison's predictions earned him the epithet 'Prophet of Doom' until his forecasts proved correct. He is now described as 'the canary in the housing mine…(his) prediction is chilling: Nostradamus...could scarcely have been more accurate."

On the other side of the pond, in the US, sits Arthur Laffer. The author of several important books on economic theory including his latest, "Return to Prosperity: How America Can Regain Its Economic Superpower Status," Laffer was also an adviser to the Reagan Administration during the 1980s and a member of the Economic Policy Advisory Board.

His economic models have been proven to work and withstood the test of time. Now Laffer has declared that the US economy is heading for a very big fall early in 2011.

The economist, best known for his economic model called the 'Laffer Curve," came to national prominence when his model was adopted by Ronald Reagan in an effort to turn the economy around after the disastrous economic policies of Jimmy Carter.

Back in the late 1970s the media kept track of 'the misery index' an informal gauge of inflation, stagnation and taxation that put a damper on the economy for years. Laffer's recommendation—to cut federal taxes significantly and roll back the rate of government spending—was employed in 1981 after Carter's bid for a second term was roundly routed by an angry American electorate.

Laffer's 'prescription' created an economic boom that carried into the Clinton presidency. It also surprised many critics of the model when it achieved what Laffer had predicted: higher revenues to the treasury despite the deep tax rate cuts.

Now Arther Laffer has analyzed the direction of the federal government over the past two years and hears alarm bells going off. The savvy economist has studied the potential impact of the historic debt, an economy hovering just above a depression, and the building pressure to raise interest rates when inflation rises in the future, and compares the ship of state to the Titanic.

"Today's corporate profits reflect an income shift into 2010. These profits will tumble next year, preceded most likely by the stock market," writes Laffer in the Wall Street Journal article, Tax Hikes and the 2011 Economic Collapse.

Laffer calls attention to the one thing that has kept the economy partially afloat, as poor as the economy has been: the Bush tax cuts. When they expire (on January 1, 2011), "federal, state and local tax rates are scheduled to rise quite sharply." Dividend tax will skyrocket from 15 percent to a whopping 39.6 percent, the capital gains tax will increase 25% and the estate tax will jump from zero to 55 percent.

These taxes—a triple whammy to the economy—will serve to further depress business growth and hiring, depress real estate further and add an even greater burden on the ability of the consumer to spend discretionary income, which will sink like a rock. To all that must be added the re-introduction of the infamous "marriage penalty" that could lead to more home foreclosures.

If all that is not bad enough, tax rates will be raised further on income earned outside the US, payroll taxes will rise in 2013 squeezing the middle-class wage earner more, the alternative minimum tax will affect people at lower income levels and taxes are scheduled to be imposed on so-called "Cadillac health care plans."

Nobel Prize winning Paul Krugman, a liberal economist, concurs, but for different reasons. He believes the federal government has not spent enough fast enough. Much of the so-called "stimulus money" authorized by Congress is languishing, unspent. Some hundred billion went to dubious projects and grants designed to stimulate nothing.

Krugman is furious. Writing in a New York Times OpEd piece recently, he condemned the current administration's economic policies and predicted a Second Great Depression. He also raised a rather bellicose alarm against Treasury and other responsible for US monetary policy—including the Fed. Krugman is convinced that tens of millions will never find work again and the economy will worsen in 2011 and 2012.

All economic indicators echo 1929 - 1933

Finally, Robin Griffiths devines the future economy from a technical market approach. Griffiths is a strategist at Cazenove Capital who recently shared with viewers of CNBC that "the world has entered significant financial depression."

According to Griffiths “Equities are for losers and bond markets for winners. Equities are simply for people who like losing money,” Griffiths said.

“A double-dip is inevitable and imminent, as Keynesian stimulus measures have never worked anywhere. We are in the equivalent of a Great Depression following 3 years of credit crisis,” he added.

Griffith has taken a seat at the economic banquet of scarcity, austerity and gloom. The entrees at that table offer very slim pickings indeed: charts depicting a 20-year economic downturn; zero growth; possible additional contraction; massive unemployment, and the imminent collapse of governments globally.

If all that's not enough, Griffiths points out that the United States' shrinking M3 money supply now matches the average decline seen from 1929 to 1933.

Despite the gloom and doom, it's best to remember that things could always be worse.

How? Well, an asteroid could hit Earth tomorrow... |

|

| |