Foreclosures Go Through the Roof

Carolyn Said - San Francisco Chronicle Carolyn Said - San Francisco Chronicle

go to original

The number of Bay Area homes lost to foreclosure during the second quarter hit the highest level in almost two decades, and the region's homeowners also received a record-high number of mortgage default notices, according to a report to be released today.

California also set a record in the April-to-June quarter for the number of foreclosures, according to DataQuick Information Systems of La Jolla. The foreclosure records date to 1988, when DataQuick began collecting such statistics.

Statewide, homeowners received the most mortgage-default notices since the fourth quarter of 1996.

What's going on?

"A combination of little or no appreciation, and, in some markets, depreciation, and some pretty funky financing that has come back to haunt some borrowers," said Andrew LePage, an analyst with DataQuick. "People used risky financing to stretch beyond their means. Now, in all likelihood, they're either experiencing payment shock because of a reset from a teaser rate, or they see (higher payments) coming and are throwing in the towel early, if they think (home) prices might go down more."

Risky mortgages, especially higher-cost subprime loans to people with poor credit or no money for down payments, became a widespread phenomenon in 2004 and 2005. Many of those loans had lower rates for the first two years that rose substantially after that.

"Folks borrowed beyond their means in larger numbers because of how common creative financing became," LePage said.

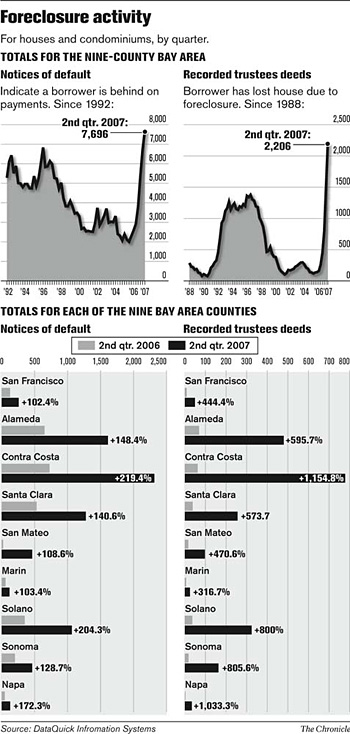

In the Bay Area, 7,696 homeowners received notices of default in the quarter, up 164.5 percent from 2,910 in the same period last year. Lenders send default notices when a homeowner is behind on mortgage payments. The notices are the first step in the foreclosure process but do not always result in foreclosure.

Several counties had the highest number of such notices since DataQuick started tracking them in 1992. Contra Costa County, with 2,316 such notices, and Solano County, with 1,065, both set records, LePage said. The Contra Costa cities of Pittsburg, Antioch and Richmond are cropping up as hot spots for foreclosures and defaults, he said. "Folks of more modest means tend to be hit the hardest."

Underscoring that thesis, three affluent Bay Area counties stood out as having the least likelihood of default notices: Marin, San Francisco and San Mateo counties.

Statewide, homeowners received 53,943 notices of default, up 158 percent from 20,909 during the same period last year. That number represents 50,901 different residences because some homes are financed with multiple loans.

California homeowners were a median five months behind on their primary mortgage before receiving the notices and owed a median $11,126 on a median $342,000 mortgage, DataQuick said. Looking at lines of credit, homeowners were a median eight months behind and owed a median $3,457 on a median $67,121 credit line.

The final step in the foreclosure process, which often comes many months after the initial default notice, is the recording of a trustee deed, meaning that the home has reverted back to the lender. In the second quarter, there were 2,206 trustee deeds recorded in the Bay Area, a 755 percent increase from 258 in the same period last year.

Statewide, the number of trustee deeds rose almost 800 percent to 17,408, compared with 1,936 in the same period a year ago. California's previous peak of foreclosures was 15,418 in the third quarter of 1996. As recently as the second quarter of 2005, the state had a record low number of foreclosures: 637. The Inland Empire and Central Valley are particularly hard hit by foreclosures.

One ominous change is that notices of default increasingly are leading to foreclosure. This year almost half - 45.4 percent - of notices of default resulted in homes being lost to foreclosure. A year ago, only 12 percent of notices of default resulted in foreclosure.

Homeowners can avoid foreclosure by bringing their payments up to date, refinancing, or selling their homes. The softening real estate market means that it is more difficult to sell or refinance. People who bought recently and financed 100 percent of their home's value cannot refinance if the home is now worth less because they don't have any equity. Similarly, if prices have fallen, they cannot sell for enough to pay off their mortgage.

"When prices were going up by double digits, anyone who fell behind on mortgage payments could stick up a 'For Sale' sign in their front yard and get enough to pay off the mortgage," LePage said.

DataQuick predicts that California foreclosures are likely to continue to climb because the conditions that lead to them still exist: rising default notices and flattening home prices.

BIG NUMBERS

-- 7,696 The number of Bay Area homeowners who received notices of default in the last quarter, up from 2,910 in the same period last year.

-- 53,943 The number of California homeowners who got notices of default, up from 20,909 from the same period last year.

-- 800 The percent increase of homes in California whose deeds reverted to bank ownership.

Source: DataQuick Information Systems

Email Carolyn Said at csaid@sfchronicle.com. |